Archive for April, 2007

Chrysler Challenge

Earlier this week there was news that Kirk Kerkorian made a $4.5B cash bid for Chrysler. Must be nice to have that much change lying around…

But to get to the point of this post, it is Easter weekend and for a couple of billion people around the globe, that means celebrating the resurrection of Jesus (or, something to do with rabbits laying colorful eggs and various chocolate treats.) But I digress. Let’s assume Kerkorian gets Chrysler from the good folks at Daimler, what should he do with it?

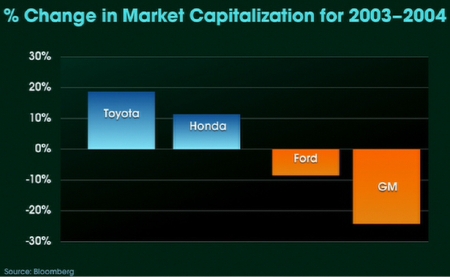

Like all American auto makers, it has a fleet of non-competitive vehicles, which coupled with rising fuel costs, is simply hammering sales. I snagged the graph below from the film An Inconvenient Truth, unfortunately, Chrysler’s market cap wasn’t on the slide since it is a subsidiary company.

It doesn’t take a Wall Street expert to interpret this chart. Fuel efficient vehicles are winning, and winning big. Last week, Toyota announced that it sold 28,453 hybrid vehicles in March. More than all of Saturn, GM’s fastest growing brand. This is not a temporary shift, it is permanent, inexorable, and accelerating.

As Easter suggests, sometimes things need to die before they can be resurrected and come back even stronger. I think that’s where the US Auto Industry is, it’s clearly dying because it is incapable of change.

Mr. Kerkorian, here’s the challenge: Don’t use half-measures, don’t compromise with hybrids. Crucify the gasoline and diesel engine. The 640hp Electric Mini project has already proved this is possible. Take the bold step forward to launch the following all electric vehicles from Chrysler:

- Full-sized pickup

- 4 door sedan

- Minivan

- Station wagon

- Coupe

Don’t get cute with this stuff, no distinctive designs, no hybrid systems, keep the range over 250 miles (400km,) and engineer the systems to use 4 motors, one on each wheel. Use your existing designs, rip the combustion engines, emissions equipment, and transmissions out and replace them with deep cycle batteries, 4 wheel mounted motors, and a 100 foot (30m) retractable extension cord. Engineer the power system to have the right performance characteristics: i.e., good low-end torque on the truck and fast acceleration on the passenger vehicles.

Get to market next year. It’s possible. What do you lose? The old market. The long haul market. But, do you care? Chrysler has lost, or is rapidly losing those markets anyway. Use your brand, your dealer network, and your manufacturing and distribution infrastructure to make this happen and to make it happen fast. And if Chrysler ultimately dies as a result of this decision? At least it went out swinging. And hey, you’re worth $15B now, you’ve still got $10B left.

This is not the time for half-measures, it’s the time for bold leadership. We’re closing factories and shipping work offshore, we’re sending billions into the middle east to fund terror each time we fill our gas tank, the temperature of the earth is quickly rising as a result of greenhouse gases. We’re facing a crisis on multiple dimensions.

Mr. Kerkorian, when you bought those surplus World War II bombers you took an enormous risk. When you built the original MGM Grand Casino, at the time, the world’s largest hotel, you took an enormous risk. You’ve got a track record, you’ve got the cash, you can do this.

The question is, will you?

Raser up 30% on private placement

Raser Technologies announced that they’ve completed a $12.5M private placement to help with drilling expenses. Traders were thrilled by this news causing the stock to climb 30%, though there has been a slight retreat since. What does this mean? In addition to the $5.5M AMP returned to Raser, there is at least $18M of cash available to Raser to funding drilling, which is phenomenally expensive.

Our unsolicited advice to the Raser team is, if you’re serious about the geothermal business (and by all indications you are,) consider buying a drill rig. With fully burdened geothermal well costs approaching $1,500/meter and the scarcity of drill rigs, this could be a solid capital acquisition that permanently reduces drilling costs by as much as 50% over the useful 30 year life of the rig.

So what did this extra money cost? The latest SEC filing indicates that Raser has 50.7M common shares outstanding. The private placement adds 2.7M shares to that total at a purchase price of $4.65 per share and grants 945,000 of warrants, essentially the right to by future shares, at a strike price of $6.05 per share. The combination of the shares and warrants (assuming they are excercised) will result in just over 7% dilution for shareholders of record at the time of the announcement.

As stated in prior entries, this is the latest in a series of deals of this type, which appears to be in vogue for geothermal developers.

Disclosure: The author holds no shares in Raser Technologies.

Consolidation time

We’ve seen a little of it already, but with hundreds of little renewable companies now operating and the bull run in the stock market showing signs of decline, consolidation should start to accelerate. It’s now time to figure out who will be acquiring and who will be targeted. The best acquirers will have a vision to fulfill and will have deep pockets (or access to deep pockets) to realize the consolidation. The targets will be predictable businesses that generate cash and carry large debt loads. Is anyone out there thinking Ormat? Calpine? Florida Power & Light?

Given the recent activity with KKR, Blackstone, and Goldman Sachs, it wouldn’t surprise me in the least if the private equity market leads this round of consolidation. Stay tuned, it’s going to be interesting.

Tesla Turbines

Atlantic Geothermal posted a link to a video by Jeff Hayes discussing Tesla Turbines. This served to remind me about these turbine/pumps and other “dead” technologies like Stirling engines. This technology is relevant as many geothermal resources have extremely high total dissolved solids (like the Salton Sea) that are expensive to harvest with conventional turbine technology.

Conventional turbines consist of a shaft with blades mounted upon it. This looks very much like closely spaced propeller blades that are pushed by pressure exerted through gas or air which causes the shaft to rotate. Conventional steam turbines have inlets near the center of a shaft with the gas/steam expanding out toward the ends with the blades becoming progressively larger from the center to the end. See the photo below of a conventional steam turbine shaft and blade assembly, the far right of the photo is where the gas/steam enters on this model and it expands and exits on the left.

Image Credit: Christian Kuhna

These turbine shaft/blade assemblies can weigh as much as 40 tons and spin at 3,600 rpm. That’s alot of mass spinning very fast. When a steam resource with high total dissolved solids is pushed through conventional turbine systems, it results in scaling, friction, and loss of efficiency. The higher the TDS, the more frequently these devices require maintenance, expensive both in absolute terms and lost opportunity.

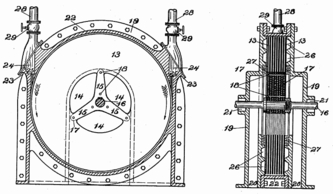

The Tesla turbine is a completely different animal. Rather than depending upon blades, it depends on centrifugal force created by adhesion of the steam/gas to large, smooth surface areas of closely spaced rotor disks. See the drawing below to get a sense of the difference between the Tesla system and conventional turbines.

Image Credit: Unknown

The figure on the left shows an end on view of the device with the shaft pointed toward the reader. One rotor is visible in this elevation with steam/gas entering on the top right of the device and exiting through the top left. Modern designs have only one inlet with the exhaust coming through the shaft region, this is important because as the rotors spin the gas is being pulled toward the shaft in a tight series of concentric circles.

The figure on the right is a side elevation of the device where the rotor assembly is the most interesting feature. These smooth disks are closely spaced (0.032″) and the adhesion of the gas/steam to the rotors cause the rotors and subsequently the shaft to rotate. The difference between conventional turbine design and the Tesla design is glaringly obvious, there is no good place for TDS to build up scaling. Another enormous difference between conventional turbines and Tesla’s design is operating speed, the Tesla, depending on rotor size, needs to operate in the 25,000 rpm realm and higher to effectively generate mechanical force. Operation at lower speeds doesn’t allow appreciable power to be harvested (which runs completely contrary to conventional turbines where power may be harvested throughout the range of rotational rpm.)

Today, Tesla turbines are used commonly as pumps for viscous materials (like crude oil) but have not found a place in turbine engine use as yet. The Department of Energy has dismissed Tesla turbines from consideration stating that “they don’t work” when compared against conventional turbines – although, this isn’t true when operated at high rpm which is the design center. So, will we see any Tesla turbines in operation? I wouldn’t bet on it in the near future, but longer term, it wouldn’t surprise me in the least to see a geothermal plant using this technology in the next 10 years.