Archive for the 'Business' Category

Ormat shares take a beating

Geothermal equipment maker and electricity producer Ormat (ORA) announced 4th quarter and 2006 full year results. Based on the run up of the stock in the early week, investors were expecting big things from this report. On Tuesday Ormat was trading at a near 52 week high of $44 per share sporting a market capitalization of $1.5B.

After results were announced Wednesday morning, shares dipped into the $37 a share range shaving market cap to $1.3B. Friday, a modest rally ensued on an upgrade from HSBC securities sending shares back to the $39 range, pretty much where the shares have been trading for the last year. Interestingly, enterprise value for the company is pegged at $1.8B so even at $44 per share, the issue was trading at a discount of $6 per share from enterprise value.

Let’s take a look at the earnings to see what we can uncover about Ormat. For the 4th quarter, the company recorded revenue of $66.7M, up from $58.8 million a year ago. Net income was $4.2M up from a loss of $5.1M a year ago, that’s a $0.28 per share swing year over year. For the year, revenues were $268.9M up from $238M a year ago and net income was $34.4M up from $15.2M a year ago. The board of directors declared a $0.07 per share dividend as well. That’s pretty impressive performance, so why did the shares get hammered?

I think it comes back to two issues: debt levels and strategy implementation. The debt is pretty straight forward, Ormat has taken on $500M in debt to finance it’s electricity generation business. Geothermal plant construction is a capital intensive business that involves the expense and risk of petro-chemical like drilling with the infrastructure requirements of traditional power plant construction. Consequently, the debt tends to be more expensive than tradition power plant construction and there tends to be alot of it per megawatt of capacity. During 2006, Ormat added 51 MW of generation capacity, bringing its total output to 377 MW.

This is a nice segue into the second issue, strategy implementation. Ormat has traditionally been a product company producing the equipment necessary to harvest power from geothermal resources. In particular, Ormat has demonstrated leadership in organic rankine cycle or binary harvest in closed geothermal systems. A few years ago, Ormat decided to get into the geothermal electricity production business in addition to its equipment business. This decision had risk of alienating their equipment customers since Ormat was now a competitor as well as a supplier in the electricity generation business.

A look into the Q4 and full year results shows that Ormat recorded equipment revenues of $20.1M and $73.5M respectively. The electricity segment shows results for Q4 and full year of $46.6M and $195.5M respectively. In the forward looking statements management indicated that equipment sales were projected to drop in 2007 while electricity segment would continue to grow. The key question is will electricity grow faster than equipment shrinks? And can Ormat continue to take on debt to finance the growth of electricity segment to fuel that growth?

The beauty of this strategy is that electricity generation is a pretty predictable business. Ormat will enter into longterm power sale agreements with known pricing and will work to control and reduce operating costs to generate predictable results. The equipment business is and will continue to be “lumpy” – dictated by the number of projects underway at any given time and with Ormat’s entry into the generation business, new competitors will appear like United Technologies with their Pure Cycle organic rankine cycle generation units.

So, what’s Ormat worth? That’s a pretty good question. Taking their generation capacity of 377 MW with average sale price of $70 per megawatt hour multiplied by the industry average capacity factor of 90% multiplied by the number of hours in the year (8760,) I would predict revenues in the electricity segment of around $208M for the full year. Management projects that the equipment segment will produce around $68M for the year. This brings projected full year revenues to $276M without the benefit of new capacity impact brought online during the year and any upside in equipment sales. However, it also takes into account a 7.5% decrease year over year in the equipment segment which may not be sufficiently pessimistic given the competitive landscape.

Provided Ormat can sustain current expense levels commensurate with revenue levels, the revenue levels above would yield earnings in the $35.3M dollar range. With a valuation of 50x earnings, which is where Ormat has been trading, that would signal a price of $52.56 per share. However, the projected earnings growth rate of 3% won’t justify that multiple. I expect Ormat’s PE will be begin to fall back toward traditional power producer multiples in the 20x range as growth slows. At a 20x valuation, that indicates a price of $19.83 per share.

If Ormat can show growth in excess of 5%, then I would expect the shares to stay closer to the high side estimate. If Ormat delivers results with 3% or less growth, I would expect quick adjustment to the lower end of the range. My conclusion is that at $35 per share, Ormat is fairly valued given the projected growth rates, risks, debt level, and strategy implementation.

If you liked this entry, Digg It!

Technorati Tags: Energy | Geothermal | Ormat

KKR led consortium acquires TXU

In what can only be described as a mega-deal, investment firm Kohlberg, Kravis, Roberts, & Co. are paying a 15% premium over market close, $69.25 per share, to take TXU Corp private. The $31.8 billion dollar deal is the largest ever to take a company private.

Why do we care? Simple, as a consequence of the takeover, TXU’s planned 11 mega-coal plants will be reduced to 3 as a result of the acquisition and stronger environmental policies are likely to be enacted. The reduction will displace some 56 million tons of carbon emissions, equivalent to preventing 10.2 million new cars from appearing on the road.

This is an interesting development to be sure. Let’s hope the focus shifts from coal to other, less polluting generation mechanisms as a private company. But axing 8 planned coal plants is a good start.

If you liked this entry, Digg It!

Technorati Tags: Energy | Megadeal | TXU Buyout

More investment in clean tech

CalPERS (the California Public Employee Retirement System) doubled down earlier this week adding $400M to the $200M already set aside for clean tech investments. This is encouraging news as it means a large investor seeking outsized returns is seeing something they like in the clean tech space as well as the simple fact that $400M more is available to entrepreneurs in the segment.

Way to go CalPERS, you’re demonstrating great leadership. Thanks to John for the pointer to this event.

If you liked this entry, Digg It!

Technorati Tags: Energy | Clean Tech | Investment

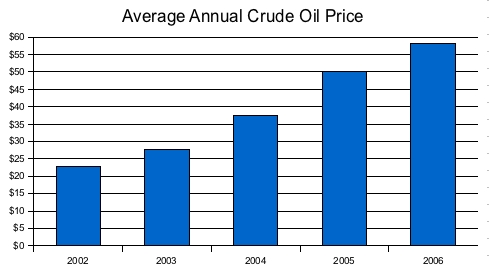

Exxon CEO says oil prices inflated by supply disruptions

In an article about world oil prices posted on CNN yesterday, Exxon CEO Rex W. Tillerson, is quoted “Crude prices in New York would be around $40-$45 a barrel without the risk of supply disruptions.” That may be true, but if we look at recent price history, that’s still 2x what crude was selling for in 2002. Check the chart below which has the average price of crude oil per barrel.

I believe that market demand, not only from the US, but globally continues to increase while supply stays relatively flat. That’s a sure fire recipe for price increase. Yes, more oil reserves are being discovered, but each successive discovery is more expensive to harvest. Make no mistake about it, oil is never going to be “cheap” again.

If you liked this entry, Digg It!

Technorati Tags: Energy | Oil Price | Supply Disruption

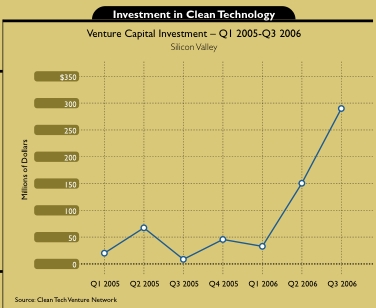

Clean tech investments increase 500%

Joint Venture of Silicon Valley publishes an annual report attempting to provide a holistic view of life and opportunity in the valley. To their credit, I’ve not seen a more complete view than what they’ve published – tip of the hat to Kevin for passing this along. The report for 2006 is available here. The report covers people, economy, society, place, and governance in the valley and is assembled by a diverse group of private and public agencies.

The general report is interesting enough, but I found a section on investment in clean tech to be very telling. Overall venture investment in the valley Quarters 1-3 in 2005 (Q4 2006 not yet available, so this will be a 3 quarter comparison) was $4.6B. The same period in 2006 saw the total rise to $5.2B, a healthy 13% increase year over year.

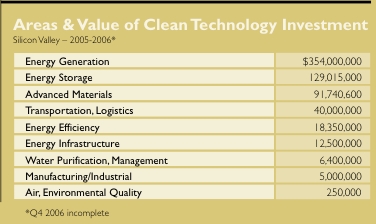

When we break out the clean tech segment, it’s even more interesting. Check the chart below:

As you can see the 2005 Q1-3 total investment was on the order of $95M compared with $480M in the same period for 2006. A 505% increase year over year. Perhaps even more importantly, the total share of clean tech in the overall venture picture increased from 2% in 2005 to 9% in 2006. The chart below gives a breakout of the general areas of investment in clean tech and the dollar amount in each category:

It’s clear that we’re starting to see a shift in the way people are thinking about “green” from something that “is good for the planet” to something that “is good business.” And that’s exactly the shift that needs to happen, until these technologies and their attendant environmental benefits are profitable, we won’t see the magnitudes of change required to make a difference. However, venture capitalists as a rule seek out places their money can work at multiples, it’s encouraging to see the expectation of returns in this segment.

If you liked this entry, Digg It!

Technorati Tags: Energy | Investment | Clean Tech